Life has a way of throwing unexpected curveballs when we least expect them. A solid emergency fund is the difference between a minor inconvenience and a financial disaster. Let me show you exactly how to build yours.

Image: Building your financial safety net

Here’s a scenario that happens more often than we’d like: Your car breaks down on Monday. The mechanic says it’s $1,200 to fix. You need that car to get to work. What do you do?

If you have an emergency fund, you transfer the money, pay the bill, and move on with your life. If you don’t? You’re looking at credit card debt, loans from family, or even worse options.

An emergency fund isn’t just nice to have – it’s absolutely essential for financial security. Yet studies show that nearly 60% of Americans couldn’t cover an unexpected $1,000 expense. That’s a scary statistic, but it doesn’t have to be you.

In this complete guide, I’ll walk you through everything you need to know about building your emergency savings: how much emergency fund you actually need, where to keep emergency fund money, and how to build it even when money is tight.

Let’s make sure you’re prepared for whatever life throws your way.

Table of Contents

What Is an Emergency Fund?

An emergency fund (also called a rainy day fund) is money set aside specifically for unexpected expenses or financial emergencies. It’s not for vacations, not for sales, not for “I really want this” moments – it’s your financial safety net for genuine emergencies only.

What Counts as an Emergency?

✅ Real emergencies:

- 🚗 Unexpected car repairs

- 🏥 Medical bills and health emergencies

- 💼 Job loss or sudden income reduction

- 🏠 Essential home repairs (roof leak, broken furnace)

- ✈️ Last-minute travel for family emergency

- 🔧 Appliance replacement (when essential)

❌ NOT emergencies:

- 🛍️ Sales or “great deals”

- 🎄 Holiday gifts (you know these are coming!)

- 📺 New TV or electronics upgrades

- ✈️ Vacation opportunities

- 👗 Clothing that isn’t essential

- 🎂 Birthday parties or celebrations

The key difference? A true emergency is unexpected, necessary, and urgent. Predictable expenses should have their own separate savings categories.

Golden Rule: Before touching your emergency fund, ask yourself: “Is this unexpected? Is it necessary? Is it urgent?” If you can’t answer yes to all three, it’s not a true emergency.

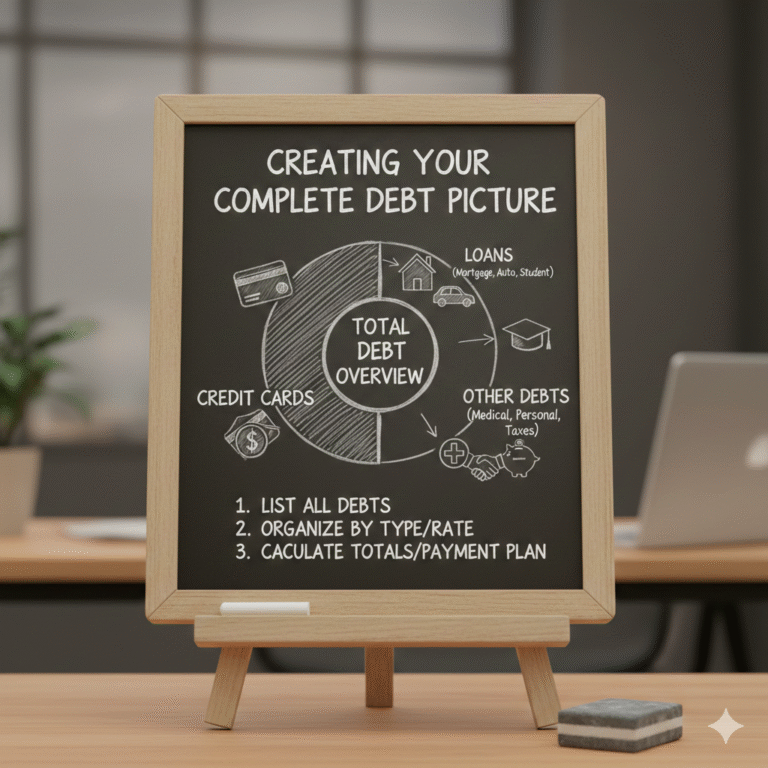

How Much Emergency Fund Do You Need?

This is the million-dollar question – or rather, the several-thousand-dollar question. The answer to “how much emergency fund” depends on your personal situation.

Image: Calculating your ideal emergency savings amount

The Standard Recommendation: 3-6 Months of Expenses

Most financial experts recommend keeping 3 to 6 months of living expenses in your emergency savings. This amount should cover all your essential costs if your income suddenly stopped.

Here’s how to calculate it:

- List all your monthly essential expenses (rent/mortgage, utilities, food, insurance, minimum debt payments, transportation)

- Add them up for your monthly total

- Multiply by 3 for minimum goal, by 6 for comfortable goal

Emergency Fund Calculator: Examples by Monthly Expense

| Monthly Expenses | 3-Month Fund (Minimum) | 6-Month Fund (Recommended) |

|---|---|---|

| $2,000 | $6,000 | $12,000 |

| $3,000 | $9,000 | $18,000 |

| $4,000 | $12,000 | $24,000 |

| $5,000 | $15,000 | $30,000 |

| $6,000 | $18,000 | $36,000 |

Related: Bankrate: Emergency Fund Calculator

Should You Save 3 Months or 6 Months?

The right amount for your rainy day fund depends on your specific circumstances:

Lean toward 3 months if:

- ✅ You have very stable employment

- ✅ You’re a dual-income household

- ✅ You have other safety nets (family support, etc.)

- ✅ Your skills are in high demand

- ✅ You have low fixed expenses

Lean toward 6+ months if:

- ✅ You’re self-employed or a freelancer

- ✅ You’re the sole income earner

- ✅ You work in an unstable industry

- ✅ You have dependents (kids, elderly parents)

- ✅ You have a chronic health condition

- ✅ Your job search would likely take longer

- ✅ You have high fixed expenses (mortgage, etc.)

Some people in particularly unstable situations even save 9-12 months. There’s no shame in having a larger cushion if it helps you sleep at night!

Where to Keep Your Emergency Fund

Knowing where to keep emergency fund money is just as important as knowing how much to save. Your emergency savings needs to be:

- Safe – You can’t risk losing it

- Accessible – You need it quickly in emergencies

- Separate – Kept away from everyday spending

Best Options for Your Emergency Fund:

1. High-Yield Savings Account (HYSA) – Best Choice for Most People

A high-yield savings account is the gold standard for emergency fund storage. Here’s why:

- 💰 Earns interest – Currently 4-5% APY at top online banks

- 🔒 FDIC insured – Protected up to $250,000

- 🏃 Accessible – Transfer to checking within 1-2 days

- 📱 Easy to set up – Most are online-only

Top HYSA providers: Marcus by Goldman Sachs, Ally Bank, American Express Savings, Capital One 360, Discover Savings

2. Money Market Account

Similar to high-yield savings, but sometimes offers check-writing ability:

- 💰 Competitive interest rates

- 🔒 FDIC insured

- ✍️ May include limited check writing

- 💵 May have higher minimum balance requirements

3. Regular Savings Account

Better than nothing, but traditional bank savings accounts offer minimal interest (often 0.01-0.1%):

- 🔒 Safe and FDIC insured

- 🏃 Very accessible

- ❌ Almost no interest earned

- 👎 Your money loses value to inflation

4. Certificates of Deposit (CDs) – For Part of Your Fund

Some people keep a portion of their larger emergency savings in CDs:

- 💰 Higher interest rates than savings

- 🔒 FDIC insured

- ⏰ Money is locked for a set term

- 💸 Early withdrawal penalties apply

Strategy: A CD ladder (multiple CDs with staggered maturity dates) can balance higher returns with some accessibility.

Where NOT to Keep Your Emergency Fund:

- ❌ Under your mattress – No interest, risk of loss/theft

- ❌ In the stock market – Too volatile; could be down when you need it

- ❌ In your checking account – Too easy to accidentally spend

- ❌ In cryptocurrency – Far too volatile for emergency needs

- ❌ In retirement accounts – Penalties for early withdrawal

Pro Tip: Open your high-yield savings account at a DIFFERENT bank than your checking. This small barrier makes it slightly harder to impulse-transfer money, protecting your rainy day fund.

Related: NerdWallet: Best High-Yield Savings Accounts

How to Build Your Emergency Fund Step by Step

Building an emergency fund from zero can feel overwhelming, but breaking it into phases makes it manageable.

Image: Building your emergency fund step by step

Phase 1: The Starter Emergency Fund ($1,000)

Your first goal is a mini emergency fund of $1,000. This covers most common emergencies:

- Minor car repairs

- Small medical co-pays

- Appliance repairs

- Unexpected travel

How to get there:

- 💵 Sell items you don’t need

- 🚫 Temporarily cut non-essential expenses

- 💰 Put all “extra” money toward this goal (tax refunds, bonuses, gifts)

- 📆 Set up a small weekly auto-transfer ($50/week = $1,000 in 5 months)

Phase 2: One Month of Expenses

Once you have $1,000, work toward one full month of essential expenses. This provides a meaningful safety net.

Phase 3: Three Months of Expenses

This is your minimum fully-funded emergency fund. At this point, you could survive a job loss for a quarter while searching for new work.

Phase 4: Six Months of Expenses

The recommended target for most people. This provides true financial security and peace of mind.

Phase 5: Beyond (Optional)

If your situation warrants it, continue to 9-12 months. Beyond that, excess money is usually better invested for growth.

Emergency Fund Calculator: Personalize Your Target

Use this emergency fund calculator framework to determine your specific number:

Image: Calculate your personalized emergency fund target

Step 1: Calculate Your Monthly Essential Expenses

| Expense Category | Your Monthly Amount |

|---|---|

| Housing (rent/mortgage) | $_______ |

| Utilities (electric, gas, water) | $_______ |

| Food (groceries only) | $_______ |

| Transportation (car payment, gas, transit) | $_______ |

| Insurance (health, car, home) | $_______ |

| Minimum debt payments | $_______ |

| Phone/internet (basic) | $_______ |

| Childcare (if applicable) | $_______ |

| TOTAL MONTHLY ESSENTIALS | $_______ |

Step 2: Apply Your Multiplier

- Very stable situation: Total × 3 = $_______

- Average situation: Total × 4 = $_______

- Less stable situation: Total × 6 = $_______

- Very unstable situation: Total × 9-12 = $_______

That final number is YOUR personalized emergency fund goal!

Tips to Build Your Emergency Fund Faster

Building emergency savings takes time, but these strategies can speed up the process:

Automate Your Savings

Set up automatic transfers from checking to your rainy day fund every payday. Treat it like a bill that must be paid. Even $25-50 per paycheck adds up over time.

Save Windfalls

Tax refunds, bonuses, birthday money, cash gifts – commit to saving at least 50% of any “extra” money that comes your way.

Cut One Expense Temporarily

Pick one discretionary expense to eliminate until your starter fund is built. Cancel a streaming service, skip dining out for a month, or pause a subscription.

Sell Unused Items

Look around your home. Old electronics, clothes you never wear, furniture you don’t need – turn clutter into emergency cash.

Round Up Purchases

Use apps that round up your purchases and save the difference. Small amounts add up surprisingly fast.

Start a Side Hustle

Dedicate all earnings from a side gig specifically to your emergency fund until it’s fully funded.

Common Emergency Fund Mistakes to Avoid

Image: Protect your emergency savings from common pitfalls

- ❌ Keeping it too accessible – If it’s in your main checking, you’ll spend it

- ❌ Not replenishing after use – When you dip in, rebuild immediately

- ❌ Using it for non-emergencies – That sale isn’t an emergency!

- ❌ Investing it in stocks – A market crash could cut it in half when you need it

- ❌ Not adjusting as life changes – Update your target when expenses change

- ❌ Waiting until you “make more” – Start with whatever you can

- ❌ Borrowing from it for “good” reasons – Even vacations aren’t emergencies

- ❌ Keeping it in a low-interest account – Why earn 0.01% when you could earn 4-5%?

Emergency Fund vs. Other Savings Goals

Where does your emergency fund fit in your overall financial priorities?

The Priority Order:

- Starter emergency fund ($1,000) – This comes first!

- Employer 401(k) match – Free money shouldn’t be left on the table

- Pay off high-interest debt – Credit cards and high-rate loans

- Full emergency fund (3-6 months) – Complete your safety net

- Max retirement contributions – Now invest aggressively

- Other savings goals – House, vacation, etc.

The reason your starter rainy day fund comes first? Without it, one emergency puts you right back into debt. It protects all your other financial progress.

Frequently Asked Questions

Is $1,000 enough for an emergency fund?

$1,000 is a good starter emergency fund, but not a fully-funded one. It covers common small emergencies but wouldn’t sustain you through job loss. Work toward 3-6 months of expenses as your ultimate goal.

Should I pay off debt or build an emergency fund first?

Build a starter emergency fund of $1,000 first, then attack debt. This prevents new debt from forming when emergencies happen during your debt payoff journey.

Can I invest my emergency fund?

No – investing your emergency savings in stocks or crypto is risky because markets can drop right when you need the money. Keep it in a high-yield savings account where it’s safe and accessible.

How long does it take to build an emergency fund?

It depends on your income, expenses, and savings rate. Saving $500/month would build a $6,000 fund in one year. Be patient – a fully-funded emergency fund is worth the effort.

Should I touch my emergency fund for large planned expenses?

No – planned expenses (even large ones like car replacement or home repairs you know are coming) should have their own savings categories. Your rainy day fund is only for truly unexpected emergencies.

What if I need to use my emergency fund?

That’s exactly what it’s for! Use it for genuine emergencies without guilt. Then make rebuilding it your top financial priority until it’s fully restored.

Final Thoughts: Your Emergency Fund Is Your Financial Foundation

Building an emergency fund isn’t the most exciting financial goal. It doesn’t grow like investments or give you the immediate satisfaction of a purchase. But it’s arguably the most important money you’ll ever save.

Here’s what a fully-funded emergency fund gives you:

- ✅ Peace of mind – You can handle whatever life throws at you

- ✅ Freedom from debt – Emergencies don’t send you to credit cards

- ✅ Better decisions – You’re not desperate when problems arise

- ✅ Opportunity – Job transitions and life changes become possible

- ✅ Better sleep – Financial anxiety decreases dramatically

Start with your first $1,000. Then keep going. One month of expenses, then three, then six. Every dollar you add to your emergency savings makes you more financially secure.

The best time to build an emergency fund was years ago. The second best time is right now.

Open that high-yield savings account today, set up your automatic transfer, and start building your financial safety net. Future you will be incredibly grateful. 💰🛡️

How much emergency fund are you working toward? Already have one fully funded? Share your experience in the comments! And if this guide helped you understand how much emergency fund you need and where to keep emergency fund money, share it with someone just starting their financial journey!