You’ve decided to tackle your debt – congratulations! That’s honestly the hardest part. Now comes the million-dollar question: what’s the best strategy to actually get it done?

If you’ve spent any time researching how to pay off debt, you’ve probably come across two popular strategies: the debt snowball vs debt avalanche methods. Both approaches have passionate supporters, and both can absolutely get you to debt freedom – but they work in completely different ways.

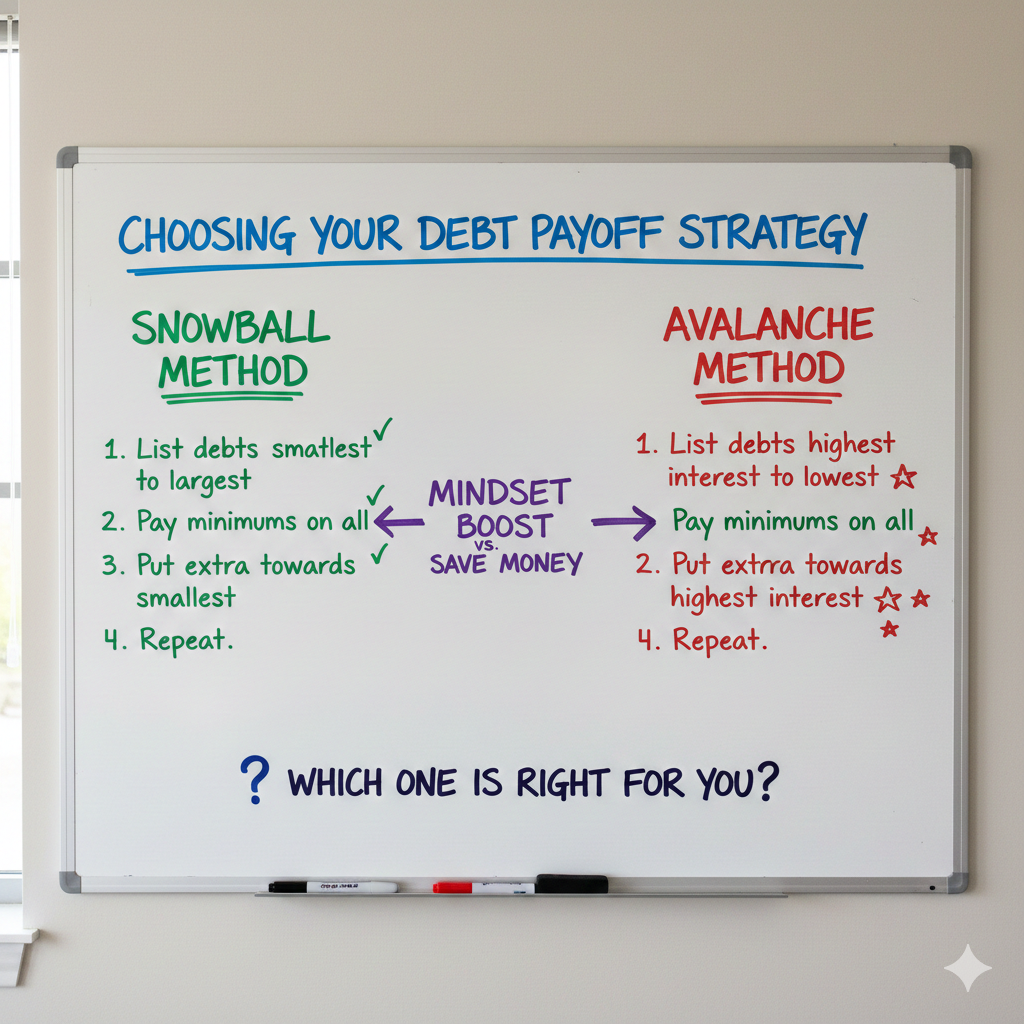

So which one is right for you? Is there actually a “better” method, or does it depend on your personality and situation?

I’ve been through my own debt free journey and helped countless friends choose between these debt payoff methods. In this comprehensive guide, I’m breaking down exactly how each method works, the pros and cons of both, and how to decide which strategy will help YOU become debt-free faster.

Let’s dive in and figure this out together.

Table of Contents

Understanding the Two Most Popular Debt Payoff Methods

Before we compare debt snowball vs debt avalanche, let’s make sure we understand exactly what each method involves. Both strategies share one common principle: you make minimum payments on all your debts, then throw any extra money at one specific debt until it’s gone. The difference lies in which debt you target first.

What Is the Debt Snowball Method?

The snowball method was popularized by personal finance guru Dave Ramsey, and it’s all about psychology over math.

Here’s how the snowball method works:

- List all your debts from smallest balance to largest balance

- Make minimum payments on everything

- Put all extra money toward the smallest debt

- Once the smallest debt is paid off, roll that payment to the next smallest

- Repeat until all debts are gone

The name “snowball” comes from the idea that as you pay off each debt, your payment amount grows larger and larger – just like a snowball rolling downhill and picking up more snow.

The Philosophy: Quick wins create motivation. When you pay off that first small debt in just a few months, you get a dopamine hit of success that keeps you going through the longer journey ahead.

What Is the Debt Avalanche Method?

The avalanche method takes a more mathematical approach to how to pay off debt. Instead of focusing on quick wins, it prioritizes saving money on interest.

Here’s how the avalanche method works:

- List all your debts from highest interest rate to lowest interest rate

- Make minimum payments on everything

- Put all extra money toward the highest-interest debt

- Once that debt is paid off, move to the next highest interest rate

- Repeat until all debts are gone

The name “avalanche” suggests the powerful force of tackling those expensive high-interest debts first, causing a cascade effect as you work through your debt list.

The Philosophy: Math doesn’t lie. By targeting the highest interest rates first, you minimize the total amount of interest you pay over time, potentially saving hundreds or even thousands of dollars.

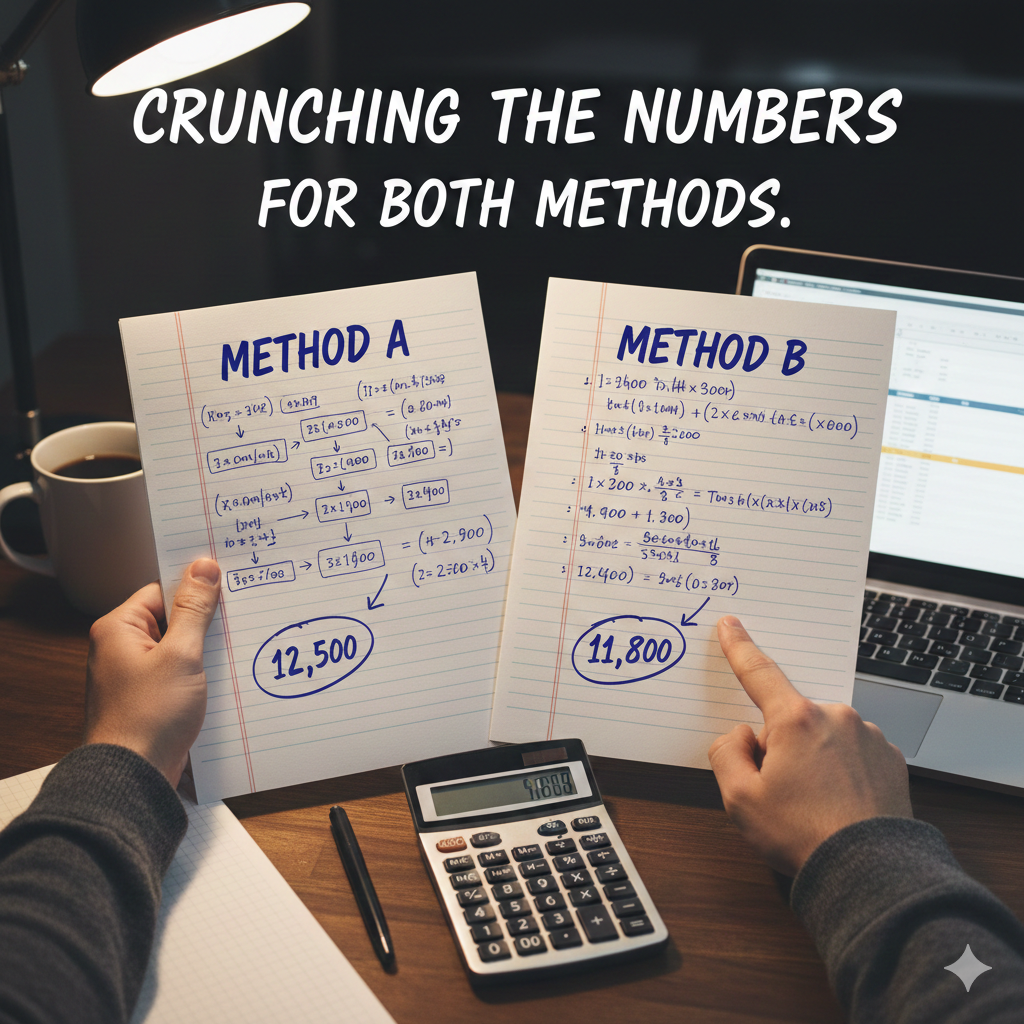

Debt Snowball vs Debt Avalanche: A Real-World Comparison

Let’s put these debt payoff methods to the test with a real example. Meet Sarah – she has the following debts and can put $500 per month toward debt repayment:

| Debt Type | Balance | Interest Rate | Minimum Payment |

|---|---|---|---|

| Credit Card A | $2,500 | 22% | $75 |

| Credit Card B | $7,000 | 18% | $140 |

| Personal Loan | $4,000 | 12% | $120 |

| Car Loan | $8,500 | 6% | $200 |

| TOTAL | $22,000 | – | $535 |

Using the Snowball Method (Smallest to Largest):

Sarah would attack her debts in this order:

- Credit Card A ($2,500) – Paid off in ~6 months

- Personal Loan ($4,000) – Paid off in ~8 more months

- Credit Card B ($7,000) – Paid off in ~12 more months

- Car Loan ($8,500) – Paid off in ~11 more months

Total time to debt freedom: Approximately 37 months

Total interest paid: Approximately $4,800

Using the Avalanche Method (Highest Interest First):

Sarah would attack her debts in this order:

- Credit Card A (22%) – Paid off in ~6 months

- Credit Card B (18%) – Paid off in ~15 more months

- Personal Loan (12%) – Paid off in ~7 more months

- Car Loan (6%) – Paid off in ~7 more months

Total time to debt freedom: Approximately 35 months

Total interest paid: Approximately $3,900

The Verdict on This Example:

| Factor | Snowball Method | Avalanche Method | Winner |

|---|---|---|---|

| Time to Debt Freedom | 37 months | 35 months | 🏆 Avalanche |

| Total Interest Paid | $4,800 | $3,900 | 🏆 Avalanche |

| First Debt Payoff | 6 months | 6 months | Tie |

| Second Debt Payoff | 14 months | 21 months | 🏆 Snowball |

In this example, the avalanche method saves Sarah $900 and gets her debt-free 2 months faster. But the snowball method gives her more quick wins earlier in the process.

The Psychological Factor: Why It Matters More Than Math

Here’s where the debt snowball vs debt avalanche debate gets really interesting. On paper, the avalanche method almost always wins. But in real life? Not so fast.

A famous study from the Kellogg School of Management found that people who focused on paying off small debts first were more likely to eliminate their overall debt. Why? Because those quick wins created momentum and motivation to keep going.

Think about it this way: starting your debt free journey is like starting a new fitness routine. You need early wins to build the habit. If your first goal is impossible to reach for two years, you’re more likely to give up.

The snowball method shines when:

- ✅ You have several small debts you can knock out quickly

- ✅ You need motivation and visible progress to stay committed

- ✅ You’ve tried to pay off debt before but lost steam

- ✅ Your interest rates are relatively similar across debts

- ✅ You’re an emotional or impulsive spender trying to change habits

The avalanche method shines when:

- ✅ You have high-interest debt (like 20%+ credit cards)

- ✅ You’re very disciplined and motivated by logic

- ✅ You can stay committed without needing quick wins

- ✅ You have a large gap between your highest and lowest interest rates

- ✅ Minimizing total cost is your top priority

Pros and Cons: Snowball Method

Let’s break down the advantages and disadvantages of this popular debt payoff approach:

Pros of the Snowball Method:

- 🎯 Quick wins boost morale – Crossing debts off your list feels amazing

- 🧠 Psychologically easier – Progress is visible and motivating

- 📉 Simplifies your finances faster – Fewer accounts to manage

- 💪 Builds momentum – Success breeds more success

- 🎓 Great for beginners – Easy to understand and implement

Cons of the Snowball Method:

- 💸 Costs more in interest – Mathematically not optimal

- ⏰ May take longer – Depending on your debt structure

- 📊 Ignores interest rates – High-rate debts grow while you focus elsewhere

Pros and Cons: Avalanche Method

Now let’s examine the mathematical favorite:

Pros of the Avalanche Method:

- 💰 Saves the most money – Less interest paid overall

- ⚡ Fastest to debt freedom – Mathematically optimal

- 🎯 Tackles expensive debt first – Stops the bleeding on high-interest accounts

- 📈 Maximum financial efficiency – Every dollar works harder

Cons of the Avalanche Method:

- 😓 Can be demotivating – Largest high-interest debt might take years

- 🐢 Slow early progress – Fewer wins to celebrate at the start

- 🧠 Requires more discipline – Must stay committed without quick rewards

- 📊 Harder to track progress – Success isn’t as visible

Related: NerdWallet: Complete Guide to the Debt Avalanche Method

Which Method Should You Choose? A Decision Framework

Still not sure which approach fits your debt free journey? Ask yourself these questions:

Question 1: How much do interest rates vary across your debts?

If your interest rates are fairly similar (within 5-7% of each other), the difference between methods is minimal. Go with snowball for the motivation boost.

If you have one debt at 24% and others at 8%, the avalanche method could save you significant money.

Question 2: What’s your personality type?

Choose Snowball if: You’re motivated by visible progress, tend to get discouraged easily, or have struggled with debt payoff attempts before.

Choose Avalanche if: You’re highly logical, patient, disciplined, and motivated by knowing you’re being mathematically optimal.

Question 3: How long will your smallest vs. highest-interest debt take to pay off?

If your smallest debt can be paid off in 2-3 months but your highest-interest debt would take 18 months, snowball might give you the wins you need to stay committed.

Question 4: Have you tried to pay off debt before?

If previous attempts failed due to losing motivation, the snowball method’s psychological benefits could be what you need to finally succeed.

The Hybrid Approach: Best of Both Worlds

Here’s a secret many financial experts don’t talk about: you don’t have to choose just one method for your entire debt free journey. Some people find success combining both debt payoff methods.

How the hybrid approach works:

- Start with snowball – Pay off 1-2 small debts quickly for momentum

- Switch to avalanche – Once motivated, tackle the high-interest debts

- Reassess periodically – If motivation drops, knock out a small debt for a win

This approach gives you the psychological boost of early wins while still prioritizing the expensive debt that’s costing you the most.

7 Tips for Success with Either Method

No matter which approach you choose for how to pay off debt, these strategies will help you succeed:

- Stop adding new debt – Cut up credit cards or freeze them (literally, in ice!)

- Build a small emergency fund first – Even $500-1000 prevents new debt from emergencies

- Automate your payments – Remove the option to skip a month

- Find extra income – Side hustles accelerate any debt payoff plan

- Track your progress visually – Use a debt tracker chart or app

- Celebrate milestones – Reward yourself (cheaply!) when you hit goals

- Stay connected to your “why” – Remember why being debt-free matters to you

Related: Dave Ramsey: How the Debt Snowball Method Works

Real Success Stories: Snowball vs Avalanche

Maria’s Snowball Success:

“I had six different debts totaling $34,000. Using the snowball method, I paid off my first three debts in just 8 months. That feeling of crossing them off was addictive! It took me 3 years total, but I never lost motivation because I always had a win coming soon.”

James’s Avalanche Victory:

“My credit card had a 26% interest rate – it was bleeding me dry. I used the avalanche method and focused everything on that card first. It took 14 months to pay off, but I saved over $2,000 in interest compared to if I’d done snowball. For me, the math kept me motivated.”

The truth? Both Maria and James became debt-free. The “best” method is the one that gets you across the finish line.

Common Mistakes to Avoid on Your Debt Free Journey

Regardless of whether you choose the snowball method or avalanche method, watch out for these pitfalls:

- ❌ Not having a budget – You can’t direct extra money to debt if you don’t know where your money goes

- ❌ Skipping minimum payments – Always pay minimums on ALL debts to avoid fees and credit damage

- ❌ Continuing to use credit cards – You’ll never get ahead if you keep adding new debt

- ❌ No emergency fund – One unexpected expense shouldn’t derail your entire plan

- ❌ Being too rigid – Life happens; adjust your plan as needed without giving up

- ❌ Ignoring the psychological factor – Choose a method that fits your personality, not just the math

- ❌ Going it alone – Share your goals with supportive friends or family for accountability

Frequently Asked Questions

Which is better: debt snowball vs debt avalanche?

Neither method is universally “better” – it depends on your situation. The avalanche method saves more money mathematically, but the snowball method provides psychological wins that help many people stay committed. The best method is the one you’ll actually stick with.

How fast can I become debt-free using these methods?

Timeline depends on your total debt, interest rates, and how much extra you can pay each month. Both methods can significantly accelerate your debt free journey compared to paying only minimum payments.

Should I include my mortgage in debt snowball or avalanche?

Most financial experts recommend focusing on consumer debt first (credit cards, personal loans, car loans) before tackling mortgage debt. Your mortgage typically has a lower interest rate and is considered “good debt.”

Can I switch between methods?

Absolutely! Many people start with snowball for quick wins, then switch to avalanche once they’ve built momentum. There’s no rule saying you have to stick with one approach forever.

What if I can only afford minimum payments?

Focus on finding ways to either cut expenses or increase income to free up extra money. Even an extra $50-100 per month makes a difference. However, if you truly can only afford minimums, still prioritize paying all minimums on time to protect your credit.

Final Thoughts: Start Your Debt Free Journey Today

The debt snowball vs debt avalanche debate has raged for years, but here’s what matters most: taking action.

Whether you choose the mathematically optimal avalanche method or the psychologically powerful snowball method, you’re making a decision to change your financial future. That’s huge.

Remember these key takeaways:

- ✅ Snowball: Attack smallest balances first for quick wins and motivation

- ✅ Avalanche: Attack highest interest rates first to save money and time

- ✅ Hybrid: Combine both strategies based on your needs

- ✅ Consistency beats perfection – Any method works if you stick with it

Your debt free journey starts with a single step. Pick a method, create your plan, and make that first extra payment today. You’ve got this!

The feeling of making that final payment and being completely debt-free? Trust me – it’s worth every sacrifice along the way. 💪💰

Still trying to decide between debt snowball vs debt avalanche? Drop a comment below with your debt situation and I’ll help you figure out which approach might work best for you! And if you found this guide helpful, share it with someone else on their debt free journey!